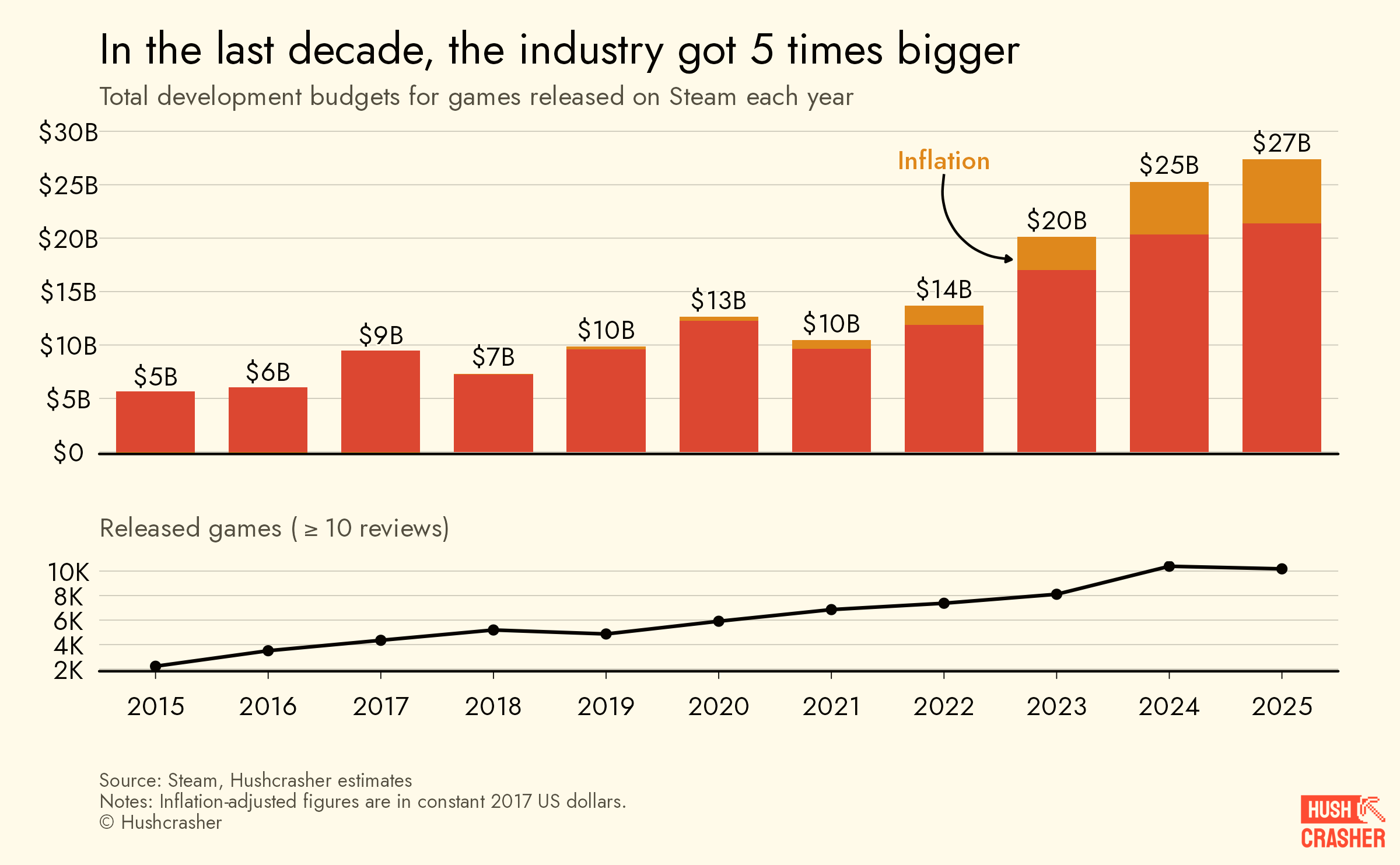

According to the Game Industry Analysis and Data Research Institute, HushCrasher, as game budgets increased with game distribution and global inflation, the total budget for the new game issued by Steam in 2025 exceeded $27 billion, compared to $5 billion in 2015, and the production costs of game developers increased 5.4 times over the past decade.Game development expenditure in 2025 was $27 billion.The game industry has never been so big. The cumulative budget for all games published on Steam in 2025 amounted to a record $27 billion, five times the figure of 10 years ago and 2.7 times that of 2019 (2.2 times the inflation adjustment). By contrast, total expenditure in the film industry in 2025 was just over $40 billion, and the entire PC game budget was equivalent to 67 per cent of the video market.

There are two possible drivers of this huge growth: an increase in game production and an increase in game costs. Distribution doubled between 2019 and 2025. This may be due to the proliferation of independent game developers during the epidemic, the first of which, in terms of time, should collide between 2021 and 2022.The cost of developing a single game soarsAverage game development costs almost doubled between 2019 and 2025. If inflation was not taken into account, the budget cost should have fallen by 28 per cent in 2025. Beginning in 2022, development costs began to rise sharply, with inflation as the main cause. This is in line with the rise in the cost of the first game, which is due to large post-epidemic investments and a two- to three-year delay in the development cycle.

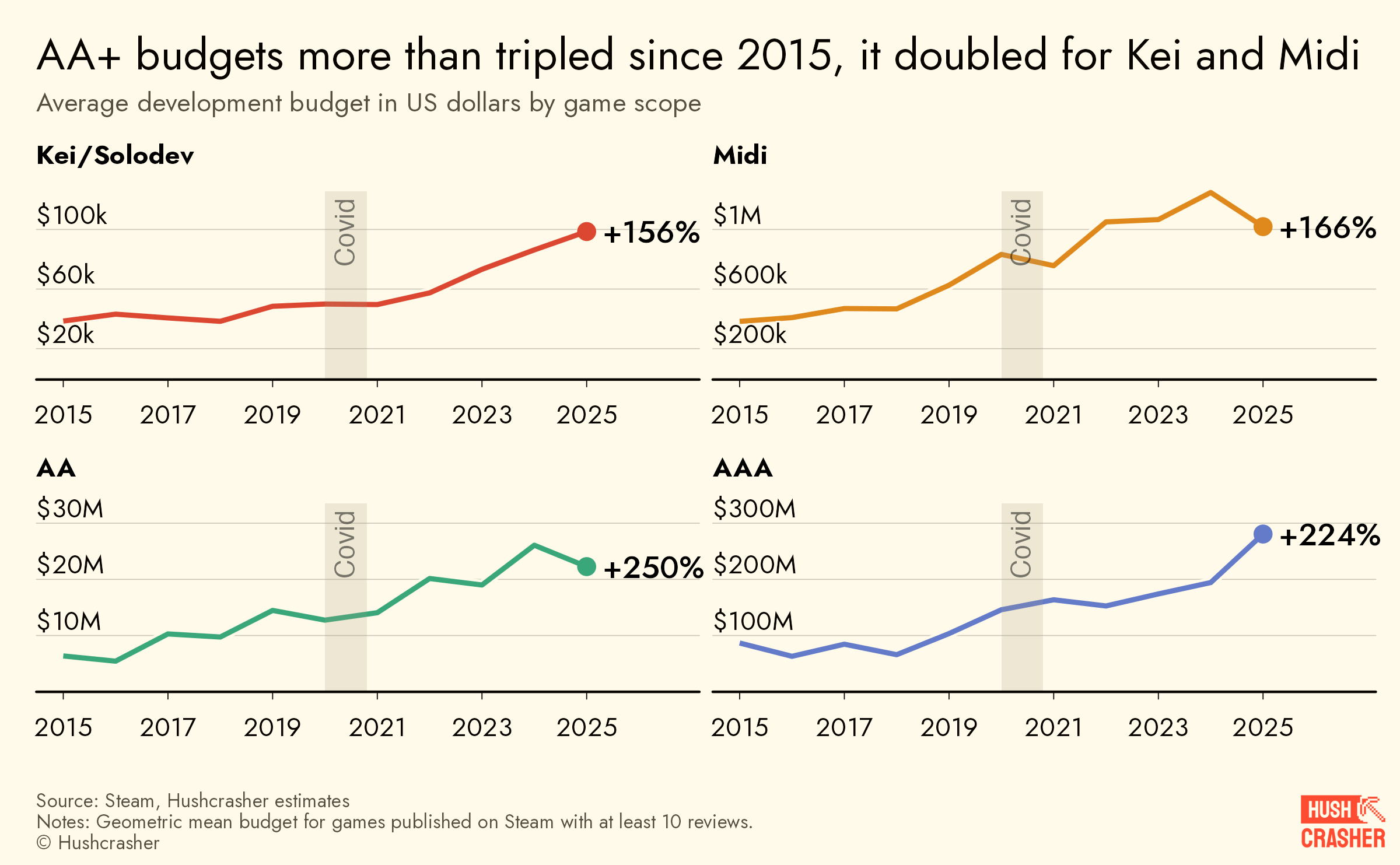

The game budget does indeed grow, but it is not just affected by inflation. The number of Kei/solodevs (light/independent developers) games has increased explosively over the past decade.Hard, long and expensive development processGame development costs are rising regardless of the size of the studio. And the bigger, the higher the increase. The budget for the development of 2A and 3A games has tripled in 10 years, while the budget for smaller games has been 2.5 times.

The Kei (light game) budget remained largely unchanged until 2021, but doubled in the following four years. After years of steady growth, the budgets for the Midi (medium game) and 2A games were all reversed in 2025, although the overall trend remained unchanged. As for the 3A game, its budget is growing in absolute terms. The single game development budget increased from about $100 million in 2019 to almost $300 million in 2025.A market environment where winners eat for all.In addition to a common explanation for the rise in labour costs, HushCrasher argues: “As the game industry increasingly moves towards a market pattern of winner-friendly food, every studio is competing for the same limited resource, the player’s attention. Once a game catches a player’s eye, other games fade out of perspective.” “This pattern, however, does not always exist. Hosted monopolistic games have spread competition to different sub-markets; marketing in the past relied on local dissemination (journalists, paper media, retail stores, etc.). This fragmentation has created space for a win-win pattern. Today, the market is moving towards a single pattern (an exception for Nintendo). Growing competition has driven every game to its head to become the ultimate winner. However, not all studios face such challenges. Small-scale and large-scale games are fundamentally different, and this is where the budget gap lies. Low-cost games emerge through horizontal differentiation (original mechanisms, unique art styles, completely new subject matter). Games such as the Ultraredisco and the Return of Oberladin have created their own exclusive course, partly avoiding competition and thus not having to invest much money.

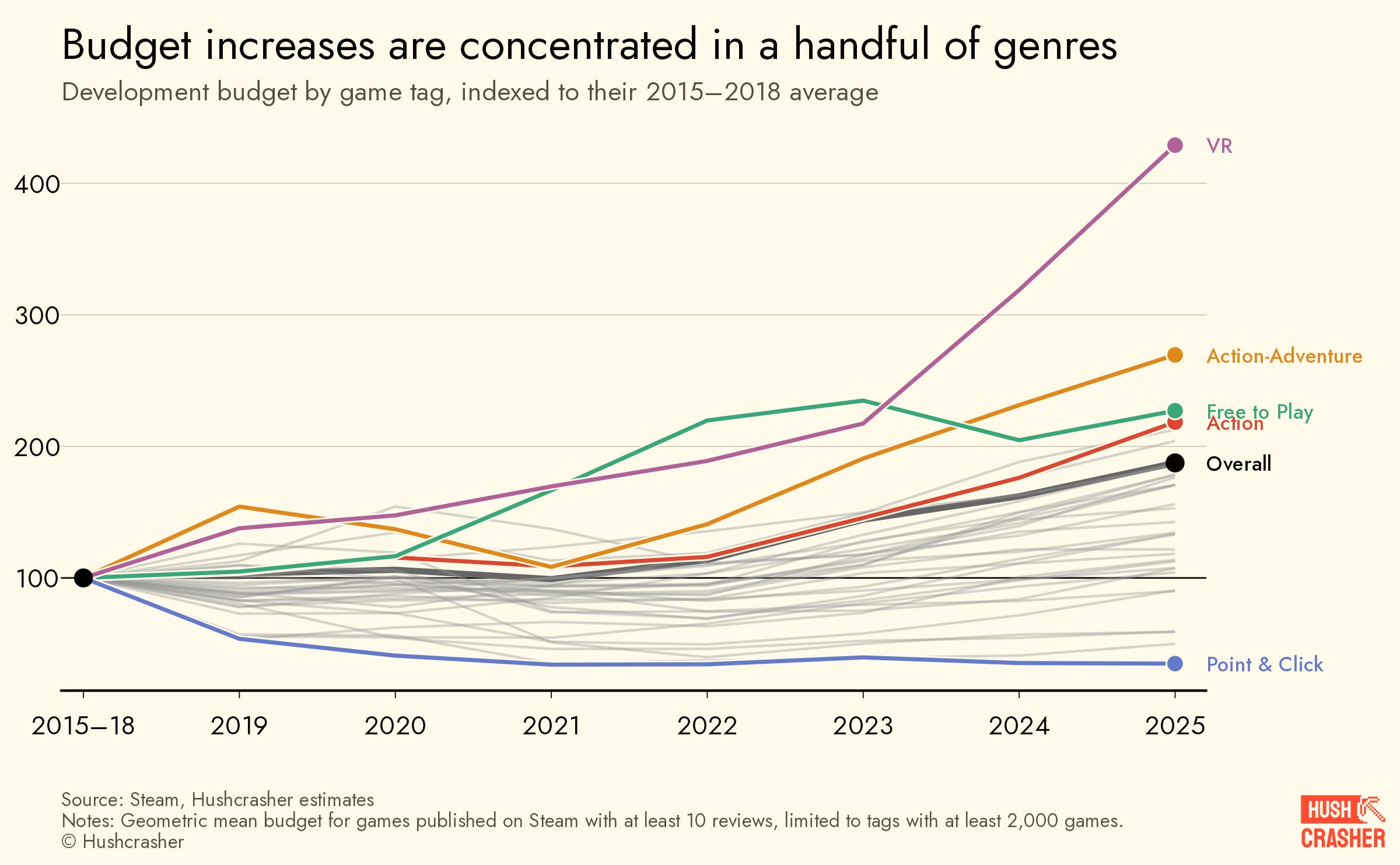

The 2A and 3A games competed in the vertical field: more content, more realistic images, and everything was escalating, creating a “inline” track where no one stepped on a brake. As a result, no efficiency improvement (better engines, more advanced AI circuits) can reduce the cost of playing, but rather contribute to the developer’s ambitions and raise the budget. In such an arms race, the cost of the game is growing explosively.Virtual reality, real cost.VR costs have increased 4.3 times in seven years and are at the top of the list. The budget remained stable until 2021, after which it began to surge. This may be due to the risk investment wave and the neural cosmology of 2021-2022, which eventually triggered the game in 2024. The rise in VR costs may not be due to the VR epidemic, but rather to the high technological costs of building a virtual reality and the expected co-benefits of the virtual world’s gold rush.

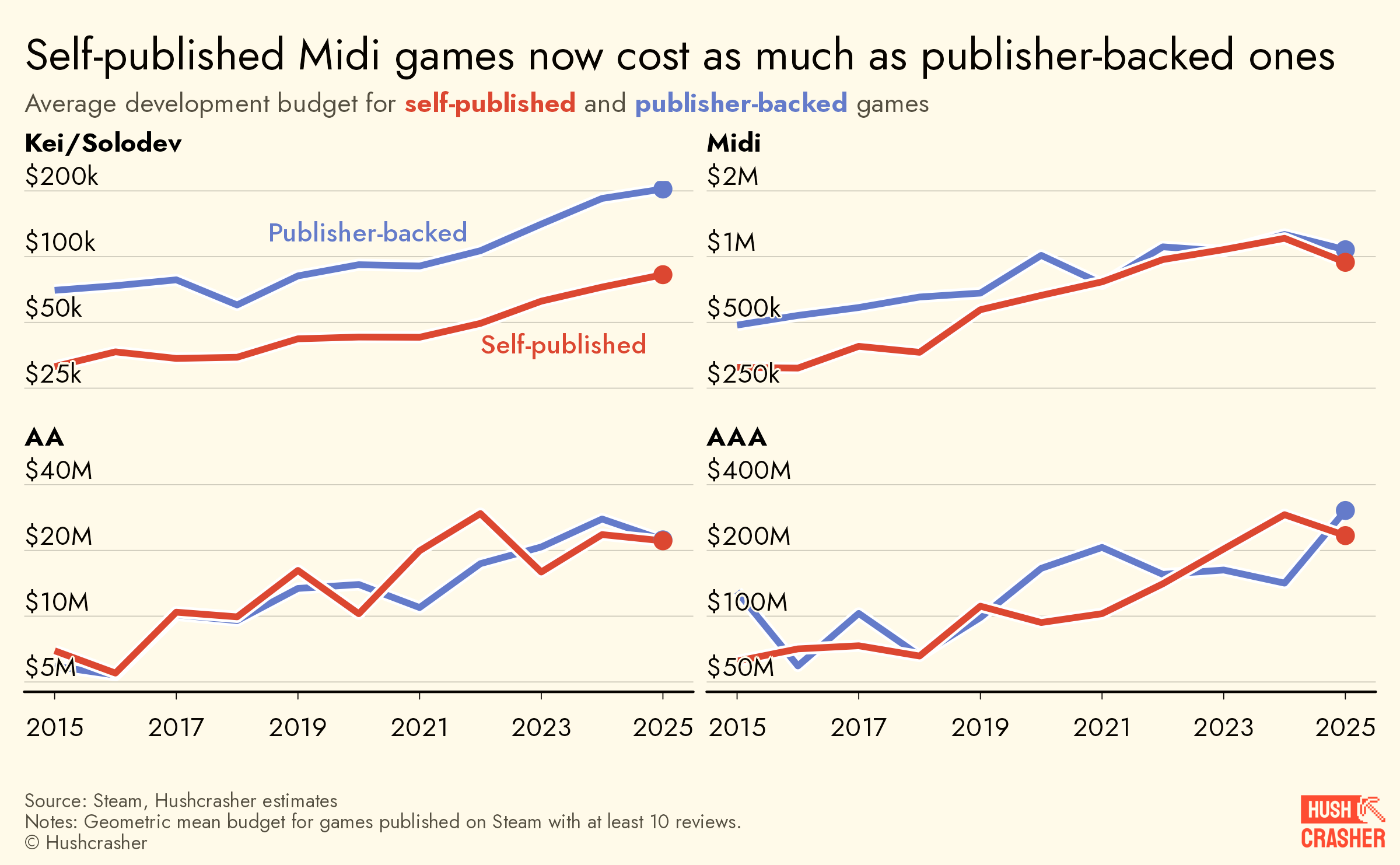

The reasons for the growth of action risk games (2.8 times more costs) and free games (2.3 times more) are different. As the most popular type of game, greater input is also needed to attract the attention of players as competition becomes more intense. On the other hand, the cost of the decryption game is reduced. Such games are now mainly made by small teams who find a way to do more or simply reduce their input. In short, budget growth has been concentrated on the most competitive and popular types.Dealer or independent?Whether or not the game is supported by a distributor not only determines who pays, but also how much it costs. For light games, the gap between distributors and game production costs remains persistent. A Kei game, supported by distributors, with a budget of approximately twice as high as that for independent production, has remained stable for many years.

Medium game is different. Although there were clear gaps in the past, they disappeared around 2021. Ten years ago, the budget for medium-sized games, supported by distributors, was approximately 1.5 times higher than for independent distribution. “The best explanation is that the role of the distributor changes when the budget exceeds a certain limit. For smaller projects, contracting with distributors can have a transformative impact. Vendors can provide localization, quality assurance, etc. More generally, there is the support of distributors to give developers more time to invest in projects to raise overall production levels.” But when the budget exceeds a certain threshold (approximately $500,000), the difference between the issuer’s funds and the developer’s self-financing becomes blurred. Below that threshold, the distributors focus on the project; when above that threshold, the distributor’s role is simply to make the project viable.” As for the 3A game, the issue of distributors was never relevant. The two curves have been interwoven over the past decade. This difference is largely man-made on the scale of the 3A game. Most of the 3A games studios are already affiliated with the issuers, either independently funded by the snowstorm or developed under the visible flag. The sector-wide budget is rising, covering all sizes, popular types and distribution patterns. However, knowing that the “budget increase” is like saying that “the patient has a fever” only sees symptoms, is unclear about the cause of the disease and does not get a prescription. However, with the widespread use of artificial intelligence and the general loss of staff, which bodes well for a reduction in the costs sought by the industry, it appears that a different picture will emerge in the future.